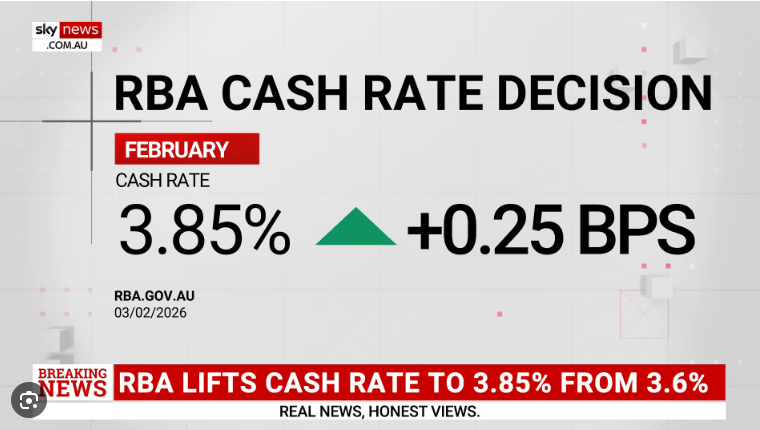

In a move that has sent ripples through the Australian property market, the Reserve Bank of Australia (RBA) decided to increase the official cash rate by 25 basis points to 3.85% at its February 3, 2026 meeting.

This marks the first interest rate hike in over two years, effectively ending the "wait and see" period of late 2025. For homeowners and property investors, this isn't just a headline—it’s a call to re-evaluate financial strategies.

Why Did the RBA Hike Rates Today?

After three rate cuts in 2025, many were hoping for continued relief. However, the RBA’s hand was forced by two primary factors:

- Sticky Inflation: Annual inflation recently jumped to 3.8%, well above the RBA’s 2-3% target band.

- Tight Labour Market: Unemployment has remained resiliently low at 4.2%, fueling wage growth and consumer spending.

RBA Governor Michele Bullock noted that while the hike might be unwelcome for mortgage holders, it is a necessary tool to prevent inflation from becoming entrenched in the economy.

1. Impact on Homeowners: The Cost of Your Mortgage

For the 3.3 million Australians with a mortgage, today’s announcement means your monthly "outgoings" are about to tick upward. Most major banks, including CBA, have already signaled they will pass the 0.25% increase on to variable-rate customers in full.

The Repayment Reality

If you have a variable-rate loan, here is what a 0.25% increase looks like in real terms:

Reduced Borrowing Power

If you were currently in the market looking to buy, your "buying ceiling" just dropped. Higher rates mean lenders will assess your serviceability more strictly, potentially reducing your maximum loan amount by roughly 2-3%.

2. Impact on Property Investors: Risk vs. Opportunity

For investors, the outlook is more nuanced. While borrowing costs are rising, the fundamentals of the Australian property market remain robust.

-

Cash Flow Squeeze: Investors with high leverage will see their interest-only or principal-and-interest repayments rise, potentially narrowing the gap between rental income and holding costs.

-

The Rental Silver Lining: As interest rates rise, homeownership becomes more expensive, often pushing would-be buyers back into the rental market. This sustained demand is expected to keep rental yields high, helping to offset increased mortgage costs.

- Tax Benefits: Remember that for investment properties, interest repayments remain tax-deductible. While a hike isn't "good" news, its impact is partially mitigated through your annual tax return.

3. Will Property Prices Fall?

History shows that while interest rates are a major factor, they aren't the only factor. Despite the hike, Australia still faces a structural supply shortage.

With population growth remaining steady and new housing completions lagging, most experts predict that property prices in cities like Sydney, Perth, and Brisbane will continue to hold firm or grow at a more moderate pace, rather than crash.

Actionable Tips for February 2026

-

For Homeowners: Check your current rate. If you haven't negotiated with your bank in the last six months, you are likely paying a "loyalty tax." Call them today or speak to a broker.

-

For Investors: Focus on high-yield markets. In a rising rate environment, capital growth is the "bonus," but cash flow is the "fuel."

- Stress Test: Ensure your budget can handle another potential 0.25% hike later this year, as the RBA has not ruled out further moves if inflation doesn't cool.

Sources

-

Reserve Bank of Australia (RBA): Monetary Policy Decision, February 3, 2026.

-

Australian Bureau of Statistics (ABS): Consumer Price Index and Labour Force data.

-

Canstar: Mortgage repayment impact analysis.

- CoreLogic: Residential property value indices.

Disclaimer

Important Notice: This article provides general information only and does not consider your personal financial situation. Property investment involves risks, including potential market volatility. We strongly recommend consulting with a qualified financial advisor, tax professional, or mortgage broker before making any investment decisions. Cubecorp Projects is not liable for any financial decisions made based on this content.